Getty Images; Tyler Le/BI

Imagine this: Just as a new generation enters the job market, a crisis rocks the world and permanently alters the economic landscape, forcing the young people starting out on their career journeys to learn the new rules of a different era. For both millennials and members of Gen Z, that description may hit close to home. Both generations were smacked with global turmoil right as they were launching their careers.

For millennials like myself, there was the financial system's implosion in 2008. Our parents lost houses, we lost our college funds, and graduated into the worst job market in at least half a century.

For Gen Zers, it was a pandemic. COVID wrecked many of your college years, and sky-high inflation ate into your meager student budgets. Now, you're out in the real world, right as the pool of entry-level jobs starts to dry up, thanks to technological change, high interest rates, and chaotic tariff policy.

Every generation has its war stories from its formative years. Gen Xers had to process 9/11 and the bursting of the tech bubble. Baby boomers dealt with their own bout of inflation and painfully high interest rates in the 1970s. But the past two upheavals felt particularly burdensome for the young generations trying to stand on their own two feet for the first time.

Today, the burden is on Gen Z after a brutal handful of years for our wallets, and society in general. Forty-eight percent of Gen Zs don't feel financially secure, according to a Deloitte survey released in June 2025, and more than 80% said their financial futures and day-to-day finances add to their anxiety and stress.

Gen Z, I hear you. I've been you. And I know there's a way through.

In these uncertain times, I'm not here to pile on the "brainrot young people" tropes or to deliver half-baked advice on how to write an effective résumé using ChatGPT. Instead, I want to provide perspective based on what we've learned time and time again over history. The US economy has gone through its fair share of triumphs and challenges, and it can feel like the deck is stacked against those of you trying to strike out on your own. But with the right conditions and careful planning, there's no doubt that all you Gen Zers out there will eventually have your moment.

Let's get one thing straight, Gen Z: you're not crazy for feeling worried about your prospects. A pandemic, political instability, social media brain rot, and two stock market crashes. Oh, and the threat of AI taking over the world and stealing all of our jobs.

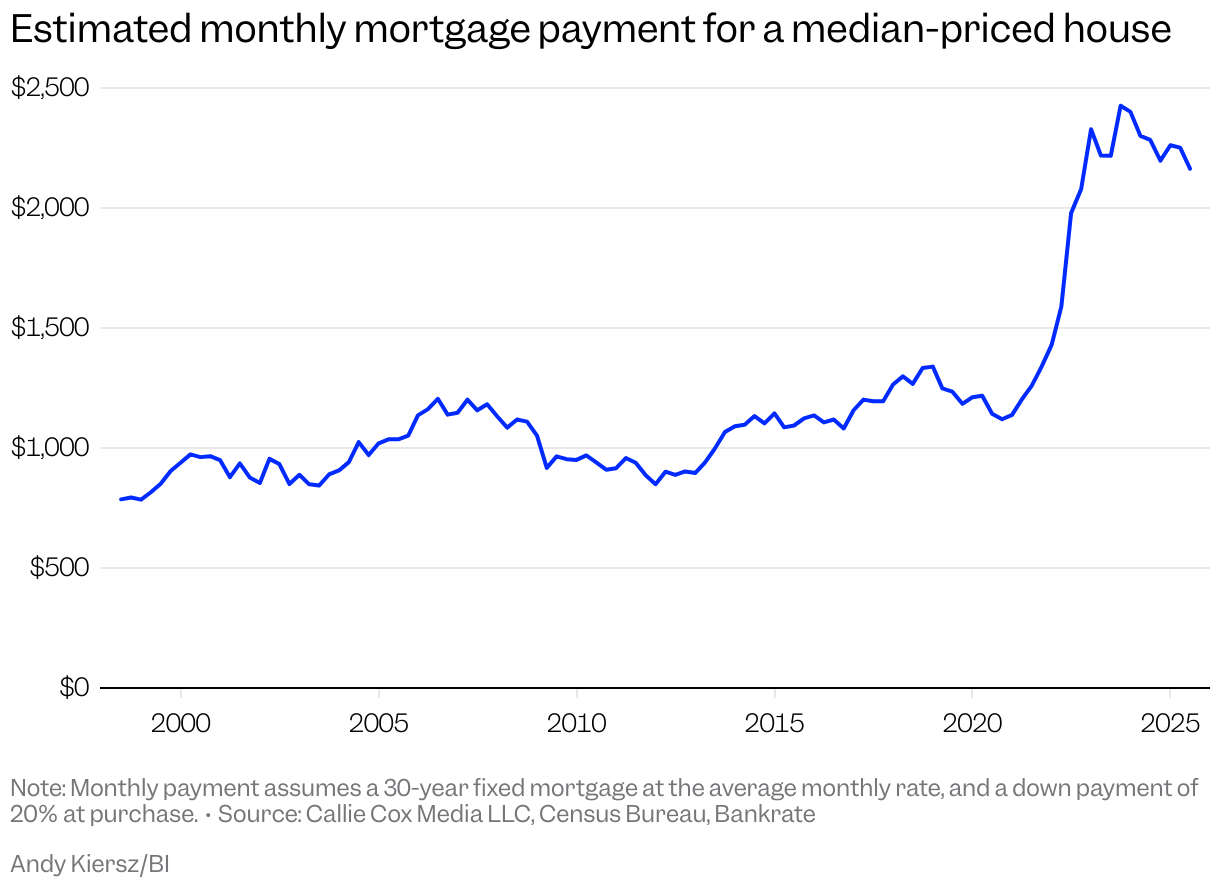

Amid all of this, we've endured an economy constantly out of balance thanks to an inflation jump not seen in four decades and the slow-motion contraction of the job market. That affordability crisis? It's absolutely a thing. There was a 17-month period between 2021 and 2023 in which paycheck growth didn't keep pace with the surge in prices. Those are just averages, too. We all know the pain of higher prices was felt more acutely depending on where you've worked and what you've purchased. Essentials like housing have become a much greater burden: Rent prices have grown faster than paychecks for much of the past 15 years, and the typical mortgage payment is almost double what it was before the pandemic.

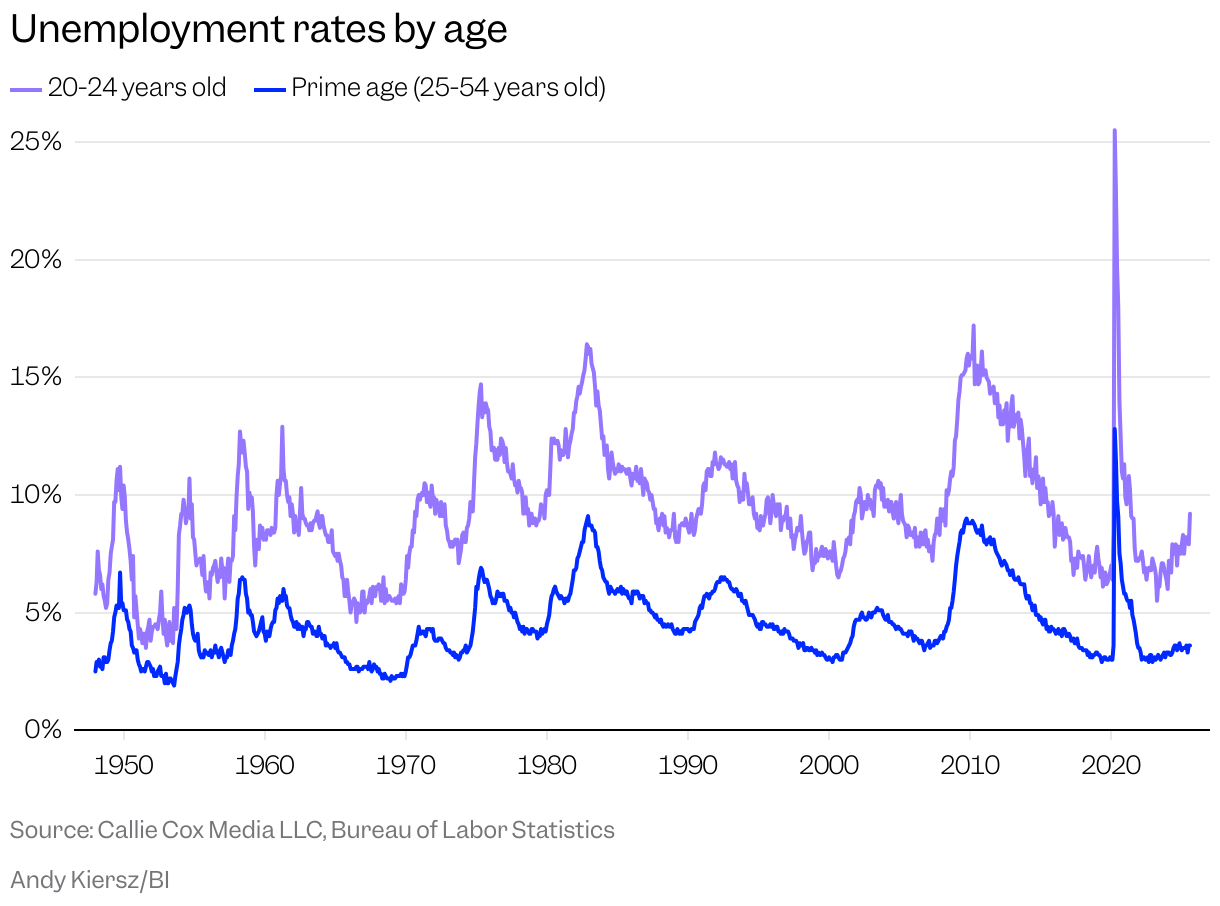

These days, paychecks are outpacing inflation again — an environment in which American households and businesses tend to thrive. But now unemployment is nipping at our heels. Especially yours, Zoomers. If you're in your early 20s, your job market prospects have soured much more quickly than for older Americans. The unemployment rate for 20 to 24 year olds is 5.6 percentage points higher than for 25 to 54 year olds (often referred to as the prime age unemployment rate because it covers a large portion of workers) — a gap so wide it's rarely seen outside economic crises.

People have been quick to point fingers at AI taking your entry-level jobs, too. Perhaps the most dispiriting part, your prospective employers are heralding this new technology not as an economic catastrophe but as a long-term structural change in how the world works and a long-term barrier to gaining on-the-job experience. And then there's Wall Street's gaslighting. Sure, society feels like it's ripping at the seams, but the stock market is trading at record highs. The dissonance between markets and large chunks of the economy is striking. Put it all together, and a bunch of you are probably feeling like you can't get off the mat. Psychologically and financially.

I didn't go through the exact same experiences you did. My senior prom wasn't canceled over a deadly virus. I didn't graduate over Zoom, and my biggest worry on social media was trying to make a new friend's top 10 ranking on MySpace. But as a millennial who graduated from high school in the depths of the financial crisis, I've felt some of the same feelings you have — even if the circumstances were drastically different.

I wasn't in the unluckiest cohort of millennials, though I wouldn't say I had it easy. I graduated from college in May 2013, when the unemployment rate for 20- to 24-year-olds was 13% — down from a then-record high of 17% for the class of 2010, but well above the current young adult unemployment rate of around 9%. I was also too young to open a brokerage account in the depths of the crisis, so I wasn't scarred forever by the pain of losing huge sums of money. Many millennials were, though. My generation is notorious for missing out on some of the best years for the stock market in recent history, simply because we couldn't — or wouldn't — invest. Our cash holdings in early adulthood were significantly higher than our Gen X predecessors, and we're the generation that brought you a thick distrust of Wall Street.

Yet I was still burned by the nasty side of risk before I was even able to start investing. My mom lost her part-time accounting job at a homebuilder after it was revealed that her company had been swindling money from customers and subcontractors. My dad was an electrician, and his business suffered under the strain of the housing market meltdown. Back then, I swore I'd never start a business. A few years later, I was tossing my résumé to anyone who would listen because I knew I needed a job ASAP. I lucked out with a great first job in one of the world's best newsrooms — an opportunity that materialized from an internship. Many of my peers weren't as fortunate, but they eventually found jobs over time.

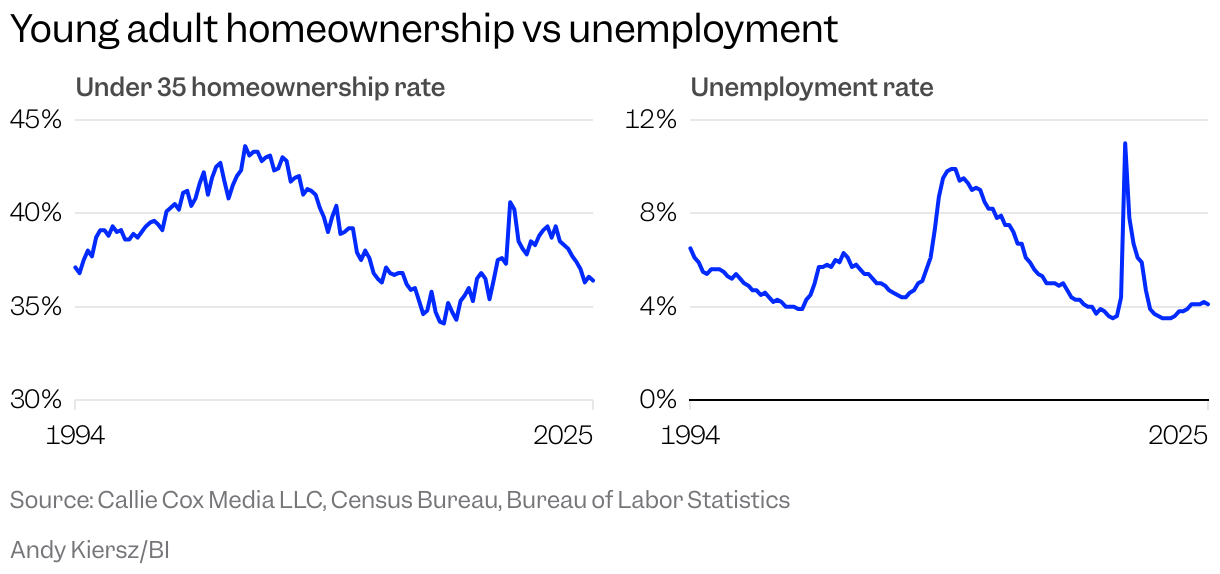

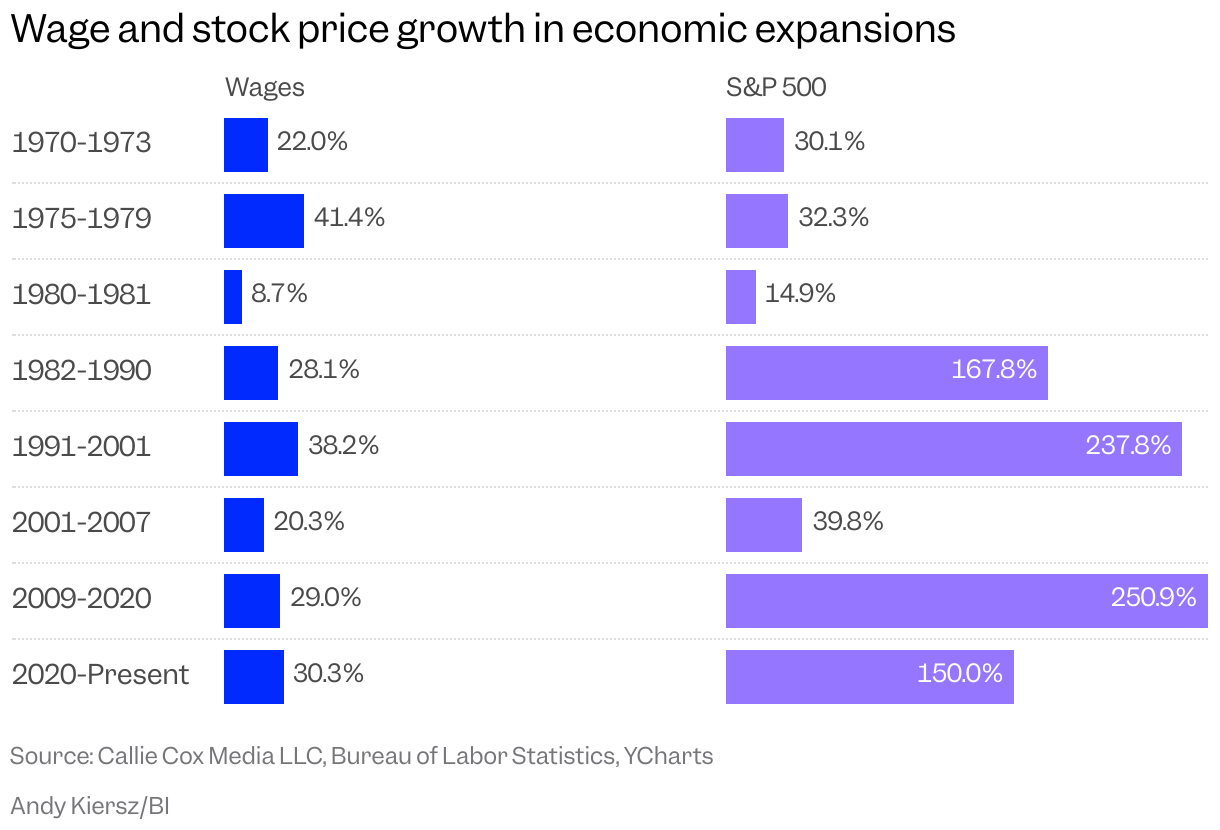

This is where I start to turn toward the sunnier news — and offer a bit of advice. Sometimes, time is all you need to heal an economic wound. You could certainly say that was true in the 2010s. Markets stopped falling, and the government stepped in to stem the economic bleeding. The unemployment rate for all ages slowly decreased over the decade, eventually reaching a 55-year low in 2019. Millennials finally felt confident enough to start investing in their 30s, catching the middle of one of the stock market's longest rallies in history — the S&P 500 nearly quadrupled from 2009 to 2020. Interest rates stayed near zero for most of the 2010s, opening the door for millennials to buy their first homes toward the end of the decade. Homeownership rates for Americans under 35 turned around in the summer of 2016, just as unemployment fell to 4% and 30-year mortgage rates reached 3.3%. And in the hot job-market days of 2022, paycheck growth for 16-24 year olds compared to all prime-age workers hit a 25-year high.

The comeback hasn't been perfect, though. Economic growth was sluggish and wages were anemic in the 2010s, which undoubtedly limited the pace of millennials' progress. Companies stopped investing in their businesses in favor of stock-boosting initiatives such as buybacks, which benefited investors more than workers. The 2010s were marked by rampant distrust of institutions, ultimately sowing the seeds for the instability we're witnessing. Millennials are still far behind Gen X and Baby Boomers in homeownership when calibrating for age, according to ApartmentList calculations of Census Bureau data.

It's easy for us older folk to step back and tell you to suck it up. Mountains of data tell us the economy ebbs and flows over time, and cycles of joy and pain are the heartbeat of the stock market. We all know words ring hollow when you're out of a job and financial stability feels unattainable.

But remember how cyclical the economy — and your fortune — can be. AI, like other technologies, may prove to be a boon for society rather than a downfall. Its cannibalization of entry-level jobs may be overstated. Sure, you could find some evidence of companies automating roles, but the slowdown in hiring looks to be more than in AI-concentrated fields. This looks more like your run-of-the-mill job market slump, something we've encountered plenty of times in history.

Economists are split on what's happening — and what comes next. Stanford researchers claim AI is already gobbling up entry-level jobs at a noticeable rate, while Yale Budget Lab analysts argue there's no evidence of this in employment and unemployment data. MIT researchers have found that a vast majority of AI implementations in businesses fail to generate profits, and a Harvard Business Review study found that AI output is actually harming worker productivity.

Everybody seems to be grasping for narratives, which appears to be a natural human response during a time of drastic change. Add in a revolutionary technology, and the noise is deafening. Right now — as it was in the late 1990s — it's hard to put a finger on what forces will prevail over the next decades. But if AI proves to be like every other technological breakthrough, it'll help us become better at our jobs and lead to lower unemployment. Yes, even if it takes years.

You can't just wait for the economic tide to pick you up, though. If we really are coming under AI's technological grip, you'll want to focus on skills that humanize you. Become a commodity in an increasingly homogenous world. Focus on empathy, communication, and strategy to set yourself apart. On the financial side, learn to be an owner, not an employee. While you initially need to make money to have money, the days of climbing the corporate ladder are long gone.

Take the last five years. The average worker's paycheck grew by 5% each year, slightly faster than the 4% growth in prices. But if you invested in a hypothetical, no-fee S&P 500 fund, you would've made 15% annual returns on your money.

This isn't a call to quit your job and become a day trader. But it is a sign of how much owners have been rewarded by technology's boon to profits and corporate America's changing incentives.

In this age of AI and rampant automation, wage growth could keep losing ground to capital appreciation, and ownership becomes even more important for your path to wealth. Especially if you think a robot could take your job.

Humans are incredibly resilient, and so far, Americans have always dug themselves out of challenging times.

Callie Cox is the chief market strategist at Ritholtz Wealth Management and the author of OptimistiCallie, a newsletter of Wall Street-quality research for everyday investors. You can view Ritholtz's disclosures here.

Read the original article on Business Insider

{kind=link}